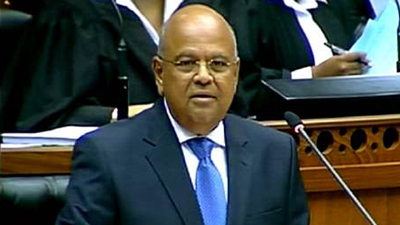

South African Finance Minister Pravin Gordhan must juggle the conflicting demands of voters and credit rating agencies this week in his first budget since he returned to the post, charged with restoring confidence in the nation’s economic management.

With South Africa threatened by ratings downgrades to “junk” status, presenting the three-year budget to parliament on Feb. 24 will test Gordhan’s political and fiscal skills to the limit.

Economic growth this year is likely to fall below 1 percent, curbing revenue just as he has to conjure up enough money to fund public sector wage rises and social program in the hope of pleasing voters before local government elections this year.

He must also persuade investors and the ratings agencies that Pretoria remains committed to budget prudence, with opponents accusing President Jacob Zuma of running Africa’s most industrialized economy into the ground through erratic policy changes that have resulted in the weak growth.

“Crunch time for South Africa’s fiscal and policy credibility comes on 24 February,” BNP Paribas Securities economist Jeffrey Schultz said. “Credit-rating agencies and markets will be keeping an eagle eye on the core details of the budget as concerns mount that the country is heading towards sub-investment-grade credit status.”

Gordhan has first-hand experience of how harshly financial markets will punish any suggestion of political machinations holding sway over economic common sense.

The rand plunged nearly 10 percent in December after Zuma suddenly fired former finance minister Nhlanhla Nene, briefly replacing him with a backbench member of parliament with no record of national fiscal management.

With the currency in free fall, Zuma backtracked rapidly, making Gordhan South Africa’s third finance minister in five days. The return of a man who earned respect at home and abroad during his first term from 2009 to 2014 helped to soothe investors at a difficult time for emerging markets.

Still, Gordhan has little room for maneuver as the budget and current account deficits are persistently running close to 5 percent of GDP while the economy has struggled to grow since a recession during the global crisis of 2008-09.

Zuma’s annual state of the nation address last week drew a cool reception, after he acknowledged that domestic structural shortcomings were partly to blame for the economic stagnation, but largely blamed a global downturn.

“Zuma (has left) all the hard work to Finance Minister Pravin Gordhan, who will face his most difficult budget presentation ever,” Teneo Intelligence southern Africa analyst Anne Fruhauf said.

The central bank has forecast growth will reach only 0.9 percent this year and unemployment is at 25 percent. The worst drought in a century is also forcing Africa’s top grain producer to import maize, while the mining industry, hit hard by slowing demand from China, is shedding jobs by the thousands.

Zuma has also hit a raw nerve with voters over a taxpayer-funded security upgrade to his private home costing 250 million rand (then $23 million). Opposition parties have asked the top court to rule on whether he broke the law. After months of denying any wrongdoing, Zuma has said he would repay the money.

“Instead of redressing the structural inequalities of apartheid, you built yourself a big house on the backs of poor South Africans,” the opposition Democratic Alliance leader Mmusi Maimane said.

The opposition is hoping public anger over the upgrade and the economy will translate into votes in municipal elections expected after May.

CHARM OFFENSIVE

Gordhan has been on a charm offensive, meeting company executives to try to repair strained relations with the African National Congress (ANC) government and calm the markets. But regaining the trust of local business, foreign investors and the ratings agencies will not be easy.

The Fitch agency cut South Africa’s sovereign credit rating in December by one notch to BBB-, the lowest investment grade category, while Standard & Poor’s kept its own BBB- rating, but changed the outlook to negative from stable.

These moves were made shortly before the episode of the three finance ministers, which drew warnings of possible further downgrades from both agencies.

Moody’s also changed its outlook on its BAA2 rating to “negative” from “stable”.

Foreign investors hold about 35 percent of South African government debt, making it vulnerable to global market sentiment and any further weakening of the rand, which lost about a quarter in value against the dollar last year.

Gordhan has promised to rein in the deficits and contain public debt below 50 percent of national output, but also faces demands from trade unions which have helped the ANC to win elections since the end of apartheid in 1994 and want money poured into the economy and creating jobs.

“Mr Gordhan needs to send a clear message to international investors and rating agencies that South Africa is committed to fiscal consolidation,” analysts at NKC African Economics said. “If, and it is a big if, he manages to do this, South Africa might manage to escape being downgraded to junk status this year.”

Gordhan may also shed light on possible sales of stakes in state-owned companies which account for about 20 percent of all capital investment. Analysts have frequently said the likes of power utility Eskom [ESCJ.UL] and loss-making South African Airways [SAA.UL] should be privatized, but the ANC has long opposed such sales.

– By